C2C vs 1099: Which Contractor Structure Actually Pays More? (2026)

December 22, 2023 | by overemployedtoolkit.com

C2C vs 1099: Which Contractor Structure Actually Pays More?

A 1099 contractor works as an individual sole proprietor and pays full self-employment tax on net earnings. A C2C (corp-to-corp) contractor invoices through their own LLC or S-Corp, which can reduce self-employment tax through reasonable salary splits, provides liability protection, and keeps the contractor’s SSN private behind an EIN.

You picked up a second remote contract. The recruiter asks how you want to be paid: 1099 or C2C? Most contractors shrug and pick whichever the agency offers by default. That shrug can cost you five figures a year once your contracting income clears six figures.

This guide is written for the person sitting on the contractor side of the table, not the employer trying to classify you. We’ll walk through the actual tax math at $100k and $150k, the disregarded LLC trap that catches almost every first-time C2C contractor, and how to structure your entity if you’re running two or three contracts at once. By the end you’ll know which structure fits your income level and how fast a C2C setup pays for itself.

What Is 1099 Contracting?

A 1099 contractor is an individual who provides services to a business as a sole proprietor. The client issues you a Form 1099-NEC at year-end reporting your gross payments. You report that income on Schedule C of your personal tax return, deduct business expenses, and pay both income tax and self-employment tax on the net profit.

The structure is dead simple. You don’t need an LLC, an EIN, a separate bank account, or an accountant. You sign the contract under your legal name, your SSN goes on the W-9, and payments hit your personal checking account. For someone testing the waters with a single short-term gig, 1099 is the path of least resistance.

The catch is the self-employment tax. As a sole proprietor you owe the full 15.3% SE tax on every dollar of net profit up to the Social Security wage base, then 2.9% Medicare on everything above. That’s on top of your federal and state income tax. The IRS explains the mechanics on its self-employment tax page, but the short version is that you’re paying both the employee and employer side of FICA out of pocket.

You also carry personal liability. If a client sues you for a deliverable that broke their production environment, they’re suing you personally. Your house, your car, your brokerage account, all of it sits inside the blast radius.

What Is Corp-to-Corp (C2C)?

Corp-to-corp means your business entity invoices the client’s business entity. You form an LLC (or sometimes a C-corp), get an EIN from the IRS, open a business bank account, and sign the contract as the LLC. The client pays the LLC, not you personally. At year-end the client issues a 1099 to the LLC if it’s taxed as a sole proprietorship or partnership, or nothing at all if you’ve made an S-Corp election.

From the agency’s perspective, C2C is cleaner. They’re contracting with another business, which sidesteps the worker-classification headache that the Department of Labor and IRS have been tightening for years. From your perspective, C2C unlocks three things a 1099 sole prop can’t touch: liability protection through the corporate veil, SE tax savings through an S-Corp election, and privacy because your SSN never appears on a vendor form.

The tradeoffs are real. You’ll spend $300 to $800 to set up the entity depending on your state, $100 to $400 a year on registered agent and state fees, and if you elect S-Corp status, $1,200 to $3,000 a year on payroll and tax prep. C2C is a business, not a side hustle, and it needs to be run like one.

C2C vs 1099 Comparison Table

Here’s how the two structures stack up on the dimensions that actually matter to a contractor making the call. If you’re also weighing a W2 arrangement against contracting, our C2C vs W2 breakdown covers that comparison in depth.

| Dimension | 1099 (Sole Prop) | C2C (LLC or S-Corp) |

|---|---|---|

| Tax structure (SE tax) | 15.3% on all net profit (up to SS wage base) | 15.3% on disregarded LLC, but S-Corp election splits salary vs distribution |

| Business entity required | None | LLC or corporation |

| SE tax savings possible | None | $5,000 to $12,000+ per year with S-Corp at $120k+ income |

| Privacy (EIN vs SSN) | SSN on every W-9 and contract | EIN only; SSN stays private |

| Personal liability protection | None; personal assets exposed | Corporate veil protects personal assets |

| Setup cost | $0 | $300 to $800 plus $100 to $400 annual maintenance |

| Good for multiple clients | Workable but mixes personal and business | Excellent; one entity invoices all clients |

| Typical rate premium | Baseline | 10% to 25% higher rates from agencies |

The Real Tax Difference: SE Tax Math

The SE tax conversation gets handwaved constantly. Let’s run actual numbers because the gap between structures is bigger than most contractors realize and smaller than the YouTube tax bros claim.

SE tax is 15.3% on the first $168,600 of net self-employment income (2024 Social Security wage base, adjusted annually) and 2.9% Medicare on everything above, plus an additional 0.9% Medicare surtax above $200k single or $250k married. You can deduct half of SE tax as an adjustment to income, which softens but doesn’t eliminate the hit. The IRS walks through the calculation on Schedule SE.

At $100k of net contracting profit as a 1099 sole prop:

- Net SE earnings: $100,000 × 92.35% = $92,350

- SE tax: $92,350 × 15.3% = $14,130

- Half SE tax deduction: $7,065 (reduces income tax, not SE tax)

- Effective SE tax cost: roughly $14,130 cash out, with $1,500 to $2,000 of income tax offset from the deduction

At $150k of net contracting profit as a 1099 sole prop:

- Net SE earnings: $150,000 × 92.35% = $138,525

- SE tax: $138,525 × 15.3% = $21,194

- That’s $21k of pure FICA on top of your federal and state income tax

Those numbers are the same whether you operate as a 1099 sole prop or as a single-member LLC without an S-Corp election. This is the trap.

The Disregarded LLC Trap

Almost every contractor who forms an LLC for the first time assumes the LLC saves them on taxes. It does not. By default the IRS treats a single-member LLC as a “disregarded entity,” which means the LLC is invisible for federal tax purposes. All income flows to Schedule C of your personal return exactly as if you were a sole prop. Same SE tax, same calculation, same $14k or $21k bill.

The LLC gives you liability protection and lets you invoice as a business, both of which matter. But it gives you zero tax savings until you file Form 2553 to elect S-Corporation taxation. We see this mistake constantly: contractor forms an LLC in January, signs C2C contracts all year, then in April discovers their tax bill is identical to last year. The election has to be filed within 75 days of formation for a new LLC, or by March 15 to apply to the current calendar year for an existing one. The IRS publishes Form 2553 with instructions for the election.

If you forgot to file on time, there’s a late election relief procedure under Rev. Proc. 2013-30 that often gets approved with a reasonable cause statement, but don’t bank on it. File the form when you form the entity.

C2C with S-Corp Election: How the Tax Savings Actually Work

Once your LLC has an S-Corp election, the tax math changes structurally. The S-Corp pays you a reasonable W-2 salary as an employee, and the remaining profit passes through to you as a distribution. Distributions are not subject to SE tax. They are still subject to ordinary income tax, but you skip the 15.3% FICA layer on that portion.

The catch is “reasonable salary.” The IRS requires that your W-2 salary reflects what someone would be paid to do your job in your market. Pay yourself $20k and distribute $130k and you’re inviting an audit. The defensible split depends on your role, market rate, and hours, but a common benchmark for senior tech contractors is roughly 50% to 65% of net business profit as salary.

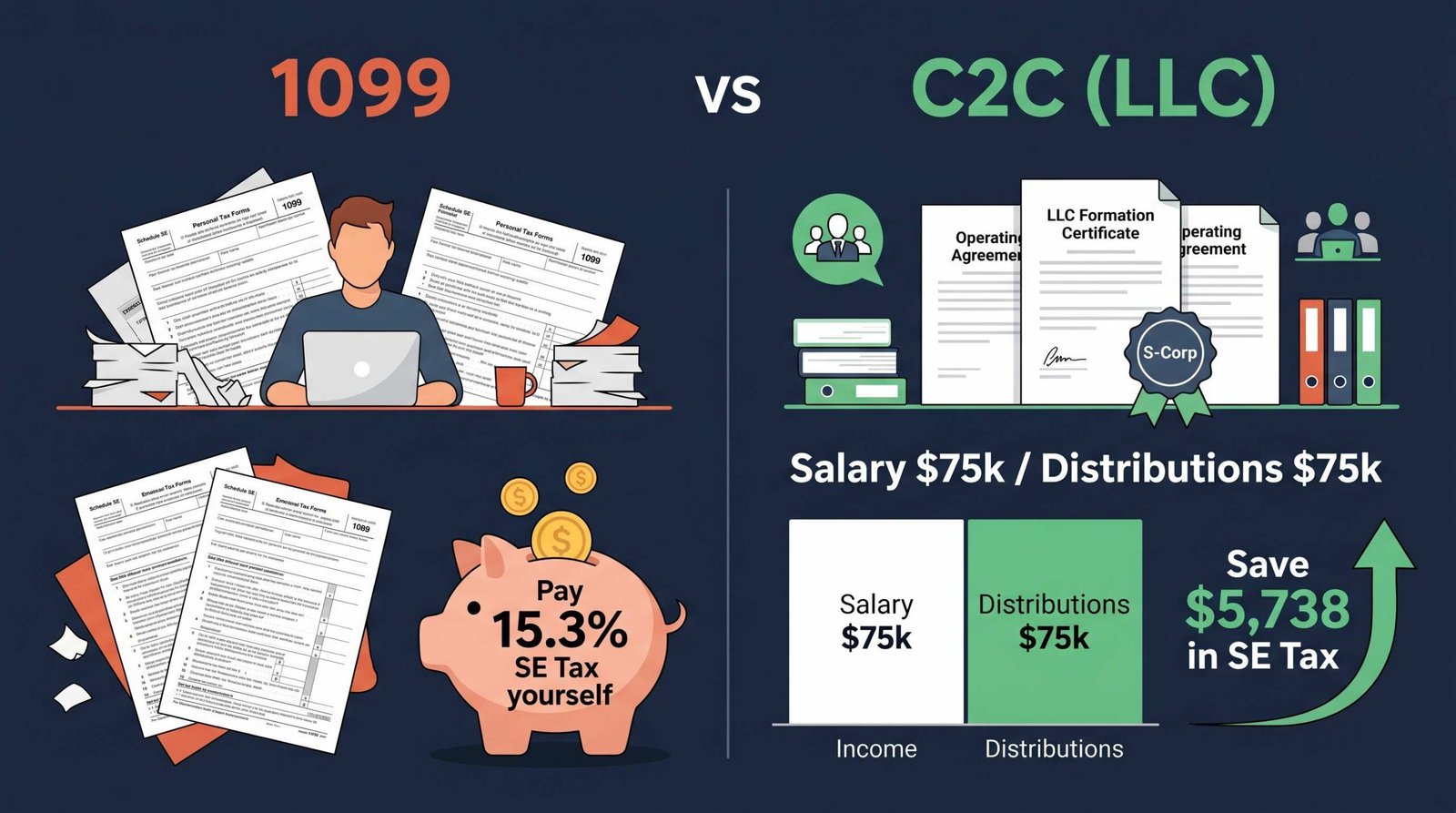

At $100k of net business profit with an S-Corp election and a $60k reasonable salary:

- W-2 salary FICA (employer + employee side): $60,000 × 15.3% = $9,180

- Distribution: $40,000 (no SE tax)

- Total FICA-equivalent: $9,180

- Savings vs 1099: $14,130 – $9,180 = $4,950

- Minus payroll and tax prep costs of roughly $1,500 to $2,500

- Net savings: roughly $2,500 to $3,500

At $150k of net business profit with an S-Corp election and an $85k reasonable salary:

- W-2 salary FICA: $85,000 × 15.3% = $13,005

- Distribution: $65,000 (no SE tax)

- Total FICA-equivalent: $13,005

- Savings vs 1099: $21,194 – $13,005 = $8,189

- Minus payroll and tax prep costs of roughly $2,000 to $3,000

- Net savings: roughly $5,200 to $6,200

The breakeven is somewhere around $60k to $80k of net business profit. Below that, the S-Corp overhead eats your savings. Above $100k, the math works clearly in your favor. Above $200k, an S-Corp is close to mandatory if you care about keeping your money.

Running Multiple Contracts from One LLC

This is where C2C earns its keep for the overemployed crowd. If you’re stacking two or three contracts, running them all through a single LLC is dramatically cleaner than juggling multiple 1099 relationships.

One entity, one EIN, one set of books, one tax return for the business. Every client invoices through the same LLC. Every payment hits the same business account. Every expense gets deducted once. At tax time your CPA pulls a single P&L and you file one Schedule K-1 or one Schedule C, depending on the entity election. Compare that to three separate Schedule C’s, three sets of expense tracking, and three 1099-NECs to reconcile, and the C2C structure starts looking like a forcing function for sanity.

The OE-specific advantage runs deeper than bookkeeping. Each client sees only your LLC name on their vendor records. They don’t see who else you’re invoicing. They don’t see your SSN. They don’t see your other contract terms. The corporate wrapper is a privacy layer that lets you operate multiple engagements without creating a paper trail any single client can pull. Worth reading our legal guide to overemployment for the broader framework on how to structure your engagements, and our breakdown of whether you can hold two full-time jobs if you’re stacking W2 and contract income.

There is one trap to flag. If two of your clients are in genuinely conflicting industries or you’ve signed exclusivity clauses with one, an LLC doesn’t override your contractual obligations. Read your contracts. A business entity gives you structural separation, not a license to breach. For the day-to-day of running multiple engagements, our guide on working two remote jobs covers the operational side.

C2C Setup Costs and Break-Even Analysis

Let’s price the C2C setup honestly so you can run the math against your contracting income.

Year-one costs for a single-member LLC with S-Corp election:

- LLC formation (state filing fee): $50 to $500 depending on state. Delaware, Wyoming, and New Mexico are common picks; your home state usually requires foreign qualification if you form elsewhere

- Registered agent: $0 if you serve yourself in your home state, $100 to $300/year if you use a service

- EIN from the IRS: free

- Operating agreement template or attorney drafting: $0 to $500

- Business bank account: free at most online banks (Mercury, Relay, Bluevine)

- Form 2553 S-Corp election: free to file yourself, $150 to $400 if a CPA does it

- Payroll service (Gusto, ADP RUN): $50 to $80/month, so $600 to $960/year

- Bookkeeping software or service: $0 to $200/month depending on whether you DIY or hire

- Tax prep for S-Corp Form 1120-S plus personal 1040: $800 to $2,500

Realistic year-one all-in cost: $1,800 to $4,000. Year-two and beyond drops to $1,500 to $3,500 since formation costs don’t repeat.

Break-even analysis: at the $5,000 to $8,000 in annual SE tax savings you can capture at $120k to $180k of net profit, the C2C structure pays for itself in year one and produces clear net savings from year two forward. Below $80k of net profit, the math gets thin and a straight 1099 setup is usually cleaner. Between $80k and $120k it’s a judgment call based on how long you plan to keep contracting and whether you value the liability and privacy benefits independent of the tax savings.

Legal Liability and Privacy

Liability protection is the underrated half of C2C. A properly maintained LLC creates a legal separation between your business and your personal assets. If a client claims your code crashed their production system and sues for damages, the lawsuit names the LLC, not you. Your personal savings, retirement accounts, and home equity sit outside the claim, assuming you haven’t pierced the corporate veil by commingling funds or signing personal guarantees.

The privacy angle matters more for OE contractors than most realize. As a 1099 sole prop, your SSN goes on the W-9 you submit to every client. That SSN sits in their vendor master file, gets accessed by AP staff, and creates discoverable links between you and each engagement. Background check services and people-search aggregators feed on this data.

With a C2C structure, your EIN is what goes on the W-9. The EIN ties to the LLC, which can be registered in a privacy-friendly state with a registered agent address that isn’t your home. Your name appears as a member or manager on state filings (and increasingly under FinCEN beneficial ownership reporting), but the day-to-day operational footprint that a client sees is purely the business entity. For someone running multiple contracts who’d rather not have an easily-searchable paper trail tying every engagement to their personal identity, this is meaningful.

A note on FinCEN: the Corporate Transparency Act requires most LLCs to report beneficial ownership information to the federal government. This data isn’t public, but it does mean the federal database knows who owns each LLC. The privacy benefit is operational, not absolute.

Benefits, Health Insurance, and Retirement

Neither C2C nor 1099 comes with employer-provided benefits. You’re buying your own health insurance, funding your own retirement, and writing your own paid time off into your billing rate. The difference is what the structure unlocks for tax-advantaged contribution vehicles.

As a 1099 sole prop, you can open a Solo 401(k) or SEP-IRA and contribute as the “employer” based on net self-employment earnings. The Solo 401(k) is the more flexible vehicle because it allows both employee elective deferrals (up to $23,000 in 2024, $30,500 if 50+) and employer profit-sharing contributions, with a combined cap of $69,000 for 2024.

As a C2C contractor with an S-Corp, you still get a Solo 401(k), but the employee deferral portion is based on your W-2 salary and the employer profit-sharing portion is capped at 25% of W-2 salary. If your reasonable salary is $60k, your max employer contribution is $15k, not 25% of total business profit. This is one of the few areas where the S-Corp election can actually reduce your retirement contribution room compared to a sole prop. Run the numbers with a CPA if you’re maxing retirement contributions, because the optimal salary for SE tax savings isn’t always the optimal salary for retirement contributions.

Health insurance is its own conversation. As a self-employed person under either structure, you can deduct health insurance premiums above the line. With an S-Corp you have to run the premiums through payroll as a fringe benefit to capture the deduction properly, which requires coordination with your payroll provider. Our guide on overemployed health insurance walks through the marketplace plans, HSAs, and group options that work best when you’re contracting through your own entity.

How to Choose: C2C vs 1099 Decision Framework

Here’s the decision flow we use when contractors ask us which structure to pick.

Is your annual contracting net profit going to be above $80k? If no, stay 1099. The C2C overhead won’t pay back.

Are you planning to contract for at least 18 to 24 months? If no, stay 1099. The setup costs amortize over multiple years.

Will you be running two or more contracts simultaneously? If yes, lean C2C even if your income is modest. The operational benefits compound when you’re juggling clients.

Do you have meaningful personal assets to protect? If yes (home equity, brokerage above $100k, kids’ 529s), lean C2C for the liability shield regardless of the tax math.

Are agencies offering you a higher rate for C2C? Many do, by 10% to 25%. If so, the rate premium often covers the setup costs by itself.

| Your Situation | Suggested Structure |

|---|---|

| Single short-term contract under $80k | 1099 |

| Single ongoing contract $80k to $120k | 1099 or LLC without S-Corp election |

| Single contract above $120k for 18+ months | C2C with S-Corp election |

| Two or more contracts simultaneously | C2C with S-Corp election |

| High personal asset exposure at any income | C2C (at minimum LLC for liability) |

Frequently Asked Questions

Does C2C pay more than 1099?

Often yes, by 10% to 25% on hourly rates. Agencies pay C2C contractors more because the engagement is cleaner from a worker-classification standpoint and the agency offloads administrative overhead onto your entity. The rate premium is on top of any SE tax savings you capture through an S-Corp election, so the total compensation advantage at higher income levels can be substantial.

Do C2C contractors pay self-employment tax?

It depends on the tax election. A C2C contractor operating as a single-member LLC without an S-Corp election pays the full 15.3% SE tax just like a 1099 sole prop, because the IRS treats the LLC as a disregarded entity. With an S-Corp election, the contractor pays FICA only on their reasonable W-2 salary; distributions are not subject to SE tax. This is the whole point of the S-Corp election.

Can I have multiple clients as a C2C contractor?

Yes, and this is one of the strongest arguments for the C2C structure. One LLC can invoice as many clients as you want, with all revenue flowing into one business bank account and one set of books. Each client sees only your LLC name on their vendor records, which gives you operational privacy across your engagements. Just make sure your individual contracts don’t include exclusivity clauses that would prohibit other work.

How do I switch from 1099 to C2C?

Form an LLC in your home state (or Delaware/Wyoming with foreign qualification), get an EIN from the IRS, open a business bank account, and file Form 2553 within 75 days if you want the S-Corp election. Then notify your existing clients that you’ll be invoicing through the LLC going forward, sign new contracts in the LLC’s name, and submit a new W-9 with your EIN. Most clients are happy to accommodate the switch mid-engagement.

Is C2C worth it for a short-term contract?

Usually not. A three-month gig at $50k of net profit won’t generate enough SE tax savings to cover the $1,800 to $4,000 of year-one setup costs. If the contract is short but you expect to continue contracting after it ends, the math works because the entity amortizes over multiple engagements. For a one-off short engagement with no plans to keep contracting, stay 1099.

What taxes does a C2C contractor pay?

Federal income tax on all business profit (whether taken as salary or distribution), state income tax where applicable, FICA on W-2 salary if S-Corp elected (or full SE tax if not elected), and any state-level franchise taxes or LLC fees. California, for example, charges an $800 annual minimum franchise tax on LLCs and S-Corps. You’ll also typically pay quarterly estimated taxes throughout the year rather than withholding from a paycheck.

The Bottom Line

The C2C vs 1099 decision boils down to income level, time horizon, and how many contracts you’re running. Below $80k of net profit on a short engagement, 1099 is the right call. Above $120k, especially if you’re stacking multiple contracts, the C2C structure with an S-Corp election pays for itself within the first year and keeps paying every year after. The privacy and liability benefits are real bonuses on top of the tax math.

The mistake we see most often is contractors forming an LLC and assuming they’ve solved the tax problem. They haven’t. The disregarded LLC pays the same SE tax as a sole prop. The S-Corp election is the actual mechanism that captures the savings, and it has to be filed on time. If you’re forming an entity this year, get the election filed within 75 days, hire a payroll provider, and run a clean reasonable salary. Done right, C2C is the most tax-efficient way to run a contracting business at the income levels most overemployed professionals operate at.

RELATED POSTS

View all

Overemployed Machine Learning Engineer: The Honest 2026 Feasibility Guide

July 1, 2026 | by Ian Adair

Overemployed Business Analyst: The Honest Feasibility Guide for 2026

December 22, 2023 | by overemployedtoolkit.com

Best Jobs for Overemployment in 2026 (Ranked by OE Feasibility)

May 13, 2026 | by Ian Adair