C2C vs W2: The Contractor’s 2026 Guide to Picking the Right Employment Type

May 21, 2026 | by Ian Adair

C2C vs W2: The Contractor’s 2026 Guide to Picking the Right Employment Type

C2C vs W2: the short version. W2 means you’re a traditional employee with taxes withheld and the employer covering half your FICA. C2C (corp-to-corp) means your LLC or S-Corp bills the client directly, you pay the full 15.3% self-employment tax, but you unlock business deductions and liability protection. C2C typically needs a 15-20% rate premium to break even financially.

If you’re choosing between a W2 offer and a C2C contract, the answer hinges on more than just hourly rate. Tax structure, benefits, deductions, and your existing income picture all factor in. And if you’re running multiple remote jobs, the calculation looks completely different than what staffing firm blogs will tell you.

This guide breaks down the real financial math, the legal mechanics, and the practical implications, written specifically for individual contractors rather than the staffing companies hiring them. We suggest reading through the breakeven math section before you negotiate any rate.

What Is W2 Employment?

W2 employment is the traditional employer-employee relationship you’ve probably had your entire working life. The company puts you on payroll, withholds federal and state taxes from each paycheck, and handles half of your FICA contribution (7.65%) while you pay the other half. At the end of the year, you receive a W2 form showing your wages and the taxes already paid on your behalf.

W2 workers are covered by unemployment insurance, workers’ compensation, and any benefits the employer offers, typically health insurance, 401k matching, paid time off, and short-term disability. The administrative load on you is minimal: file your taxes annually, deduct what you can, done.

This is the standard arrangement for the vast majority of full-time remote jobs, and it’s how most overemployed workers structure their primary income. Predictability is the main selling point. The trade-off is less flexibility, fewer deductions, and someone else controlling how and when you’re paid.

What Is Corp-to-Corp (C2C)?

Corp-to-Corp means your business entity contracts with another business entity. You set up an LLC or S-Corp first, then your company bills the client company for your services. The client never pays you personally, they pay your LLC, which then pays you as an owner-employee or distributes profits to you.

The setup work is real. You’ll need to form the LLC with your state, get an EIN from the IRS, open a business bank account, and depending on your state, file annual reports and pay franchise taxes. Most contractors going C2C also hire a bookkeeper or accountant to handle quarterly filings and year-end taxes.

In exchange, you get a layer of liability protection between your personal assets and your business activities, access to business deductions that W2 workers can’t touch, and the ability to control how income flows through your entity for tax optimization. For high earners with significant deductible expenses, C2C frequently nets more take-home than an equivalent W2 rate.

C2C vs 1099: What’s the Difference?

People conflate these constantly. Here’s the cleanest distinction: 1099 means you as an individual are contracting directly with the client. The client issues you a 1099-NEC at year-end showing what they paid you, and you report that income on Schedule C of your personal tax return. There’s no separate business entity involved.

C2C means your business entity is the contractor. The client signs an agreement with your LLC, pays your LLC, and at year-end issues a 1099 to your LLC (or sometimes no 1099 at all if you’ve elected S-Corp taxation and operate as a corporation). Both arrangements are self-employed for tax purposes, but C2C adds a corporate veil between you and the client. If something goes wrong with the engagement, the client is contracting with your business, not with you personally.

For overemployed workers specifically, this distinction matters. A 1099 arrangement still shows up under your Social Security number. A C2C arrangement shows up under your LLC’s EIN, which adds a meaningful privacy layer.

C2C vs W2 at a Glance

| Factor | W2 Employment | C2C (Corp-to-Corp) |

|---|---|---|

| Tax responsibility | Employer withholds; you file annually | You handle quarterly estimates and annual filings |

| Who pays FICA | Split 50/50: 7.65% employer, 7.65% you | You pay the full 15.3% as self-employment tax |

| Benefits | Health, 401k match, PTO, disability typical | None, you arrange your own |

| Setup required | None, sign offer letter and start | LLC formation, EIN, business bank account |

| Billing arrangement | Salary or hourly paycheck on regular cadence | Invoice the client; payment terms net 15 to net 45 |

| Liability protection | Employer carries it | LLC shields personal assets from business claims |

| Job security | At-will, but unemployment insurance applies | Contract-based, no unemployment coverage |

| Deductions available | Standard or itemized only | Full Schedule C business deductions |

| Quarterly filing | Not required | Required if you owe over $1,000 in tax |

| Typical rate premium needed | Baseline | 15 to 25 percent above W2 equivalent |

The Real Financial Math: C2C vs W2 Pay Rates

This is where most contractor blogs lose the plot. The headline rate on a C2C contract usually looks bigger than a W2 offer, but that gap can disappear fast once you account for taxes and benefits. Let’s walk through it properly.

The Self-Employment Tax Premium

On a W2, your employer pays 7.65% of FICA (Social Security plus Medicare) and you pay the matching 7.65%. The total is 15.3%, but half is invisible to you because it never appears on your paycheck. The employer just covers it.

On C2C, you pay the full 15.3% yourself. This is the self-employment tax (Social Security and Medicare) portion of your tax bill, and it applies to your net business earnings, not gross revenue. The 12.4% Social Security portion is capped at the wage base ($176,100 for 2025; the 2026 figure adjusts slightly), while the 2.9% Medicare portion has no cap and an additional 0.9% surtax kicks in above $200,000 of earnings.

The partial offset: you can deduct 50% of your self-employment tax from your gross income on Form 1040 when calculating adjusted gross income. This doesn’t eliminate the SE tax itself, but it does reduce your federal income tax bill, softening the blow somewhat.

Business Deductions That Change the Math

This is where C2C gets interesting. As an LLC owner, you can deduct legitimate business expenses against your gross revenue before calculating your taxable income. We’re talking home office (a portion of rent or mortgage, utilities, internet), vehicle expenses for business travel, equipment like computers and monitors, software subscriptions, professional development courses, conference fees, and health insurance premiums if you’re self-employed and not eligible for coverage through a spouse or another W2 job.

These deductions get reported on Schedule C (Form 1040) if you’re a single-member LLC taxed as a sole proprietorship, or on Form 1120-S if you’ve elected S-Corp taxation. Either way, the net effect is reducing your taxable income substantially. A contractor with $200,000 in C2C revenue and $40,000 in legitimate business expenses only pays self-employment tax and federal income tax on the $160,000 net.

W2 employees cannot deduct any of this. Unreimbursed employee expenses were eliminated by the Tax Cuts and Jobs Act in 2018, so even your home office goes uncompensated tax-wise if you’re a W2 remote worker.

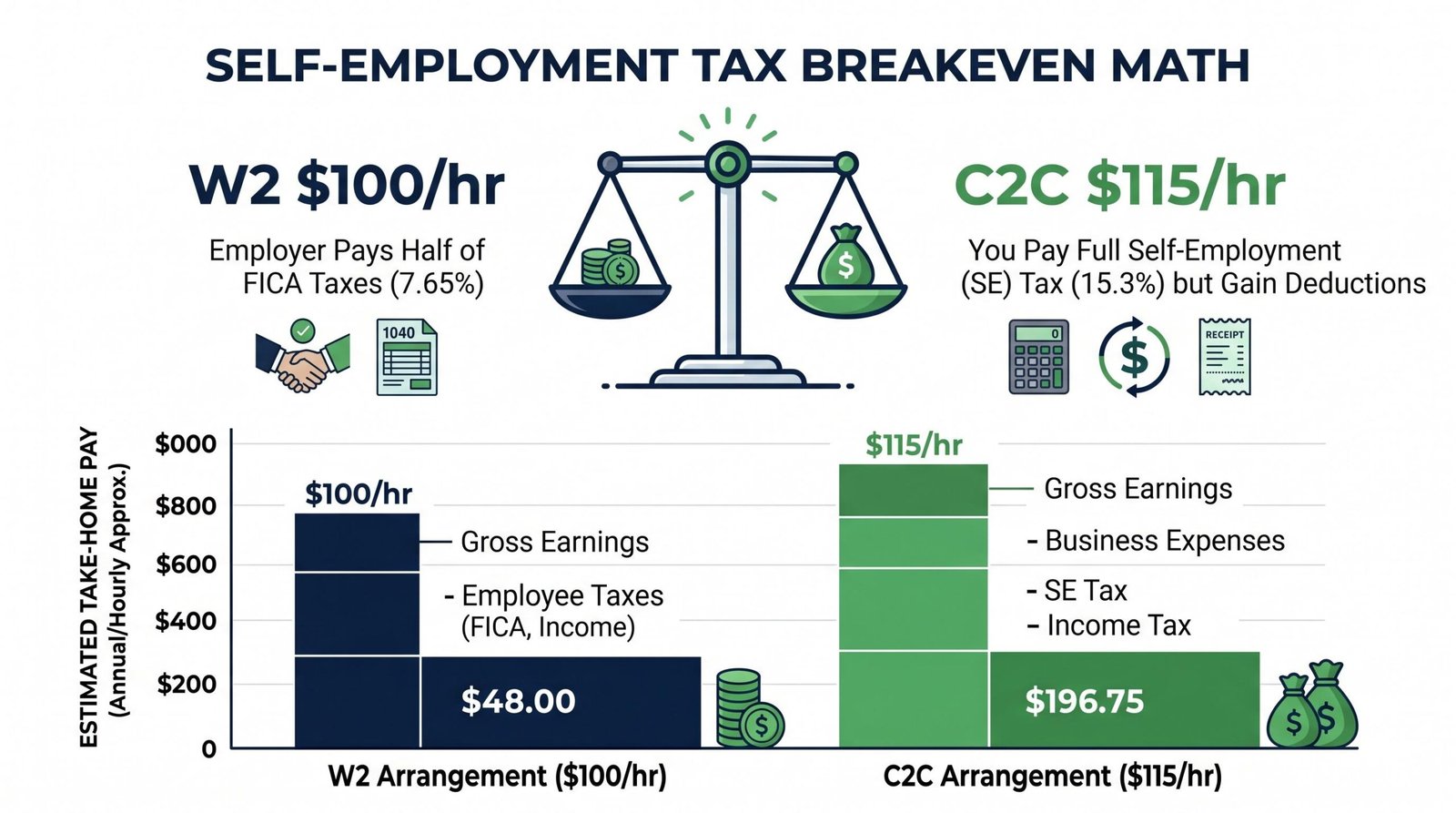

The Breakeven Rate: How Much More You Need on C2C

Let’s run a real example. A W2 offer comes in at $100 per hour, full-time, with health insurance, 401k match of 4%, and three weeks PTO. A C2C contract offers $115 per hour, no benefits.

On the W2 side at 2,000 paid hours per year: $200,000 gross. The employer is also paying roughly $15,300 in FICA (employer side), maybe $18,000 in health insurance premiums, $8,000 in 401k match, and the PTO is built into your paid hours. Effective total compensation is closer to $241,000.

On the C2C side at 2,000 billable hours: $230,000 gross revenue. You pay 15.3% SE tax on net earnings (call it $30,000 in deductions, so SE tax on $200,000 net is about $28,200, with half deductible). You buy your own health insurance ($18,000), fund your own retirement (potentially more than the W2 match through a Solo 401k or SEP-IRA), and lose income for any time off. Take-home math depends heavily on what you can deduct, but at this premium, the C2C contractor frequently ends up roughly even or slightly behind unless deductions are substantial.

The premium typically needed to break even on C2C is 15 to 20 percent over a W2 equivalent, sometimes more. The exact premium varies based on your income level, your deduction profile, and whether you’re already getting benefits from another W2 job. That last variable is where overemployed workers gain a structural edge that most contractor calculators completely miss.

Benefits and Protections: What You Give Up Going C2C

Going C2C means losing the employer-sponsored safety net. No more employer-paid health insurance, no 401k match, no PTO, no sick leave, no unemployment insurance if the contract ends, and no workers’ compensation if you injure yourself in your home office.

Health insurance is the big one for most contractors. Marketplace plans for a healthy 35-year-old run $400 to $800 per month depending on state and plan tier. For a family of four, you’re easily looking at $2,000+ per month. That said, if you have a W2 job providing coverage, this entire concern evaporates. You’re paying nothing extra for the C2C contract.

Retirement is more flexible than people realize on C2C. A Solo 401k lets you contribute as both employee and employer, with a combined limit that frequently exceeds what you’d contribute through a W2 plan. SEP-IRAs allow contributions of up to 25% of net self-employment income, capped well into the five-figure range annually. The lack of an employer match is real, but the higher contribution limits often more than compensate for it if your income supports it.

Unemployment insurance is a genuine loss. If your contract ends abruptly, you have no claim on unemployment benefits in most states. This is one reason holding a W2 anchor job alongside C2C work is structurally smart, the W2 job provides the unemployment backstop while the C2C contract maximizes income.

C2C vs W2 When You’re Overemployed

Most C2C vs W2 articles ignore the scenario where you’re running both simultaneously. For overemployed workers, this combination is one of the most powerful income structures available, and almost nobody writes about why.

The privacy advantage is substantial. When a client pays your LLC instead of you personally, the contract income flows through your business EIN rather than your SSN. This makes it materially harder to detect on standard background checks, which typically pull employment history tied to your SSN through services like The Work Number. Your LLC’s contracts don’t show up there. Knowing whether is overemployment legal in your situation matters before you start, and the structure of your contracts affects how visible your additional income is.

Holding a W2 job and a C2C contract simultaneously is legal and common in the OE community. Your W2 employer doesn’t have any inherent right to know about your business entity unless you’ve signed a moonlighting clause or non-compete that specifically prohibits it. Even then, the disclosure obligation usually only kicks in when the contract directly conflicts with your W2 duties. Most people working two remote jobs simultaneously structure one as W2 (the anchor with benefits) and the other as C2C (the high-rate variable income).

Tax strategy gets interesting fast. Your W2 wages run through standard withholding and you can’t deduct much against them. Your C2C income flows through your LLC and unlocks the full Schedule C deduction set, home office, equipment, software, professional development, the works. You’re running two parallel tax structures at once, optimizing each for what it’s good at.

If you already have health insurance from your W2 job, one of the biggest C2C drawbacks disappears entirely. You’re not paying $1,000+ per month for marketplace coverage, you’re just adding C2C revenue on top of an existing benefits structure. The same logic applies to 401k access, disability insurance, and life insurance if your W2 employer provides those. For specifics on coverage decisions, see our guide on health insurance for overemployed workers.

Quarterly estimated taxes become essential when you have C2C income alongside W2 wages. The IRS expects you to pay as you earn, and underpayment penalties apply if you wait until April. You’ll need to file quarterly estimated tax payments (Form 1040-ES) on the standard schedule: April 15, June 16, September 15, and January 15 of the following year. Many overemployed C2C workers increase their W2 withholding to cover the quarterly obligation rather than cutting separate checks, which simplifies cash management.

For workers earlier in the OE journey, our guide on how to become overemployed covers the foundational steps before you start mixing employment types.

When C2C Makes More Sense Than W2

C2C is the right call when you already have W2 benefits from another job, especially health insurance and 401k access. The biggest financial drawbacks of going independent disappear when an existing employer is already covering them.

It also makes sense when the rate premium is genuinely sufficient. A 15% premium above the W2 equivalent rate is the minimum we suggest considering. Anything less, and you’re probably trading benefits for nothing meaningful.

Privacy is a legitimate reason to prefer C2C. If you want your contract income tied to your LLC’s EIN rather than your personal SSN, C2C is the only way to achieve that cleanly. Background check services don’t typically surface LLC-level activity, so this matters for OE workers managing visibility carefully.

And if you have significant business expenses you can legitimately deduct, home office, vehicle, equipment, software, courses, conferences, the deduction stack tilts heavily in favor of C2C. A contractor with $40,000 in real annual business expenses is leaving substantial tax savings on the table by accepting W2 instead.

When W2 Makes More Sense Than C2C

W2 wins when this is your only income source. You need the health insurance, the 401k match, the unemployment coverage, and the predictable paycheck. Without an anchor benefits structure, going pure C2C carries real financial risk if anything disrupts the contract.

It also wins when the rate premium is insufficient. If a C2C offer is only 5 to 10% above the W2 equivalent, the math almost certainly favors W2 once you factor in self-employment tax, benefits replacement, and administrative overhead. Don’t talk yourself into worse compensation just because the headline rate looks bigger.

W2 is simpler if you don’t want quarterly filings, business banking, bookkeeping, and the general administrative load of running an entity. Some contractors genuinely don’t want to be small business owners. That’s a valid preference and W2 respects it.

For short engagements (under six months), the setup overhead of forming an LLC usually isn’t worth it. By the time you’ve registered the entity, opened the bank account, and gotten the paperwork in order, the contract is half over. W2 or 1099 is cleaner for short-term work.

Frequently Asked Questions

Is C2C the same as 1099?

No, but they’re related. 1099 means you as an individual are contracting directly with a client and receiving a 1099-NEC at year-end. C2C means your business entity (LLC or S-Corp) is the contracting party and the client pays your entity. Both are self-employed arrangements for tax purposes, but C2C adds liability protection and changes how the income shows up on background checks. You file Schedule C on your personal return for both, unless your LLC has elected S-Corp taxation.

Do I need an LLC to work C2C?

Yes. The “corp” in corp-to-corp refers to a corporate entity, which means an LLC, S-Corp, or C-Corp. Most contractors choose a single-member LLC because setup is simple, ongoing compliance is light, and you can elect S-Corp taxation later if your income justifies it. Forming an LLC typically costs $100 to $500 depending on the state, plus annual fees that range from $0 to a few hundred dollars.

How much more should I charge on C2C vs W2?

We suggest a minimum 15% premium above the W2 equivalent rate, with 20 to 25% being the more comfortable target once you factor in self-employment tax, benefits replacement, and administrative overhead. If you already have W2 benefits from another job, you can accept the lower end of that range because you’re not replacing benefits you don’t need. If C2C is your only income, push for the higher end.

Can I work W2 and C2C at the same time?

Yes, and this combination is one of the most powerful income structures for overemployed workers. The W2 job provides benefits, unemployment coverage, and predictable income. The C2C contract adds variable high-rate income with full deductions and privacy through your LLC. Just check your W2 employer’s policies on outside work, particularly any non-compete or moonlighting clauses. Our guide on working two full-time jobs at once covers the legal and practical mechanics in detail.

What taxes do I pay on C2C income?

You pay self-employment tax (15.3% on net earnings, half of which is deductible on Form 1040), federal income tax at your marginal rate, and state income tax if your state collects it. If your net earnings exceed $200,000 (or $250,000 married filing jointly), an additional 0.9% Medicare surtax applies. You’re also expected to make quarterly estimated tax payments throughout the year using Form 1040-ES to avoid underpayment penalties.

Is C2C better for overemployed workers?

Frequently yes, particularly as your second or third income stream after you’ve established a W2 anchor job. The privacy advantage (income tied to your LLC’s EIN rather than your SSN), the deduction stack (home office, equipment, software, professional development), and the absence of additional benefits you don’t need (because your W2 already covers them) all favor C2C. The main exception is short engagements where setup overhead isn’t worth it. For longer contracts at solid rates, C2C is typically the smarter structure once you’re already overemployed.

RELATED POSTS

View all

Health Insurance When You’re Overemployed: What to Do With Multiple Plans

May 12, 2026 | by Ian Adair

Overemployed Machine Learning Engineer: The Honest 2026 Feasibility Guide

July 1, 2026 | by Ian Adair

Overemployed and Fired: What Actually Happens (And How to Protect Yourself)

December 22, 2023 | by overemployedtoolkit.com