Health Insurance When You’re Overemployed: What to Do With Multiple Plans

Working two full-time jobs legally creates a problem that single-jobbers never face: you now have access to two health plans, two sets of premiums, two networks, and a tax question that can quietly cost you thousands of dollars a year. The Reddit threads usually stop at “yes, you can have both.” That answer is technically correct and practically useless. The real decision involves coordination of benefits, primary vs. secondary payer rules, and one HSA rule that disqualifies you from a tax-free account the moment you check the wrong enrollment box.

This guide walks through every common OE setup, the math behind picking one plan vs. two, and the HSA trap that most articles on this topic skip entirely.

When you’re overemployed, you can enroll in health insurance from multiple employers. Your J1 plan typically becomes your primary insurance and J2 becomes secondary, covering some remaining costs. The critical caveat: if either plan is an HDHP (High Deductible Health Plan), enrolling in a second plan disqualifies you from contributing to an HSA.

Do You Have to Take Health Insurance From Every Job?

No. Employer health coverage is voluntary. You can decline it at hire, decline it at open enrollment, or drop it during a qualifying life event window. No employer is going to ask why, and nothing on a W-2 or pay stub flags whether you accepted coverage at another company.

Most people getting started with overemployment keep J1’s plan and decline J2’s, for a simple reason: a single plan is cleaner, the premium is lower, and there are no coordination of benefits headaches at the provider’s billing office. We suggest this as the default unless you have a specific reason to pick something else.

Taking both plans makes sense in narrower situations:

- J2 has dramatically better coverage (lower deductible, broader network, a specialist in-network that J1 excludes).

- You expect a high-cost year (planned surgery, a baby, ongoing specialist care) and want secondary coverage to absorb out-of-pocket costs.

- One of the J’s offers an unusually cheap premium because of generous employer subsidies, and the marginal cost of carrying both is small.

- You’re worried about J1 ending suddenly and want J2 already active so there’s no gap.

If none of those apply, decline J2 health benefits and move on. Use the time you save to focus on holding down both jobs instead of optimizing a 1% margin on healthcare costs.

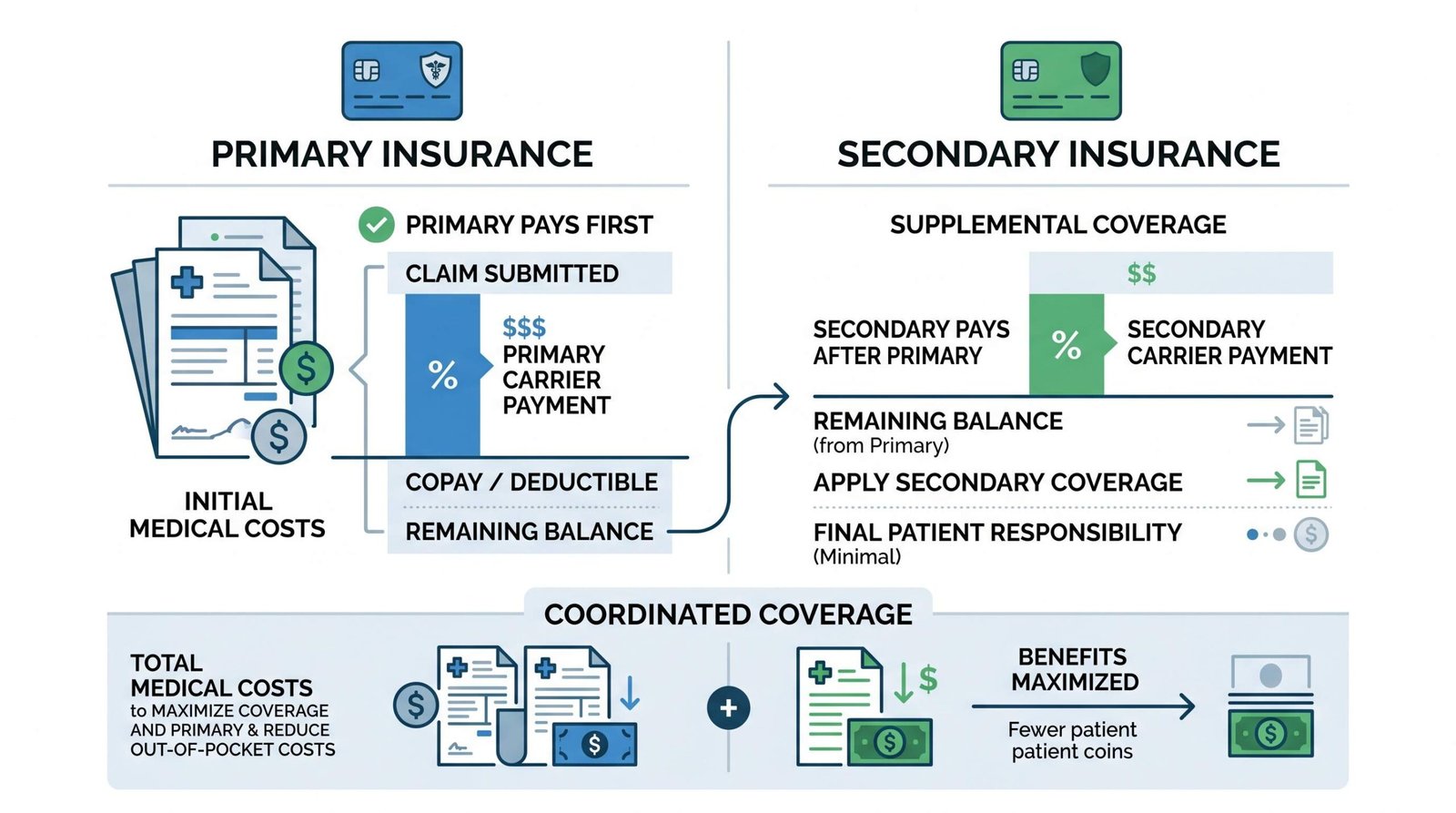

How Primary and Secondary Insurance Works With Multiple Jobs

When two health plans cover the same person, insurers use coordination of benefits to decide who pays first. The primary plan pays its share against the claim. Whatever’s left, the secondary plan considers. If the secondary plan would have covered more than the primary on that claim type, it can pick up part of the remainder. If it would have covered less, it pays nothing.

The order is set by rule, not by you:

- Your own employer plan is primary for you over a spouse’s plan that lists you as a dependent.

- The “birthday rule” decides whose plan is primary for a child covered by two parents: the parent whose birthday falls earlier in the calendar year is primary. Year of birth doesn’t matter, only month and day.

- For two of your own employer plans, the plan in effect longer is generally primary. So your J1 plan, which started first, is normally primary; J2 is secondary.

Here’s what coordination actually looks like in practice. Assume a $1,000 in-network claim, both plans have a $30 copay model after deductibles are met:

- One plan only: Plan pays $970. You pay the $30 copay.

- Two plans: J1 pays $970 as primary. The remaining $30 goes to J2 as secondary. J2 sees the claim, sees the patient responsibility is $30, and applies its own copay logic. In a clean case, J2 pays the $30. You pay nothing.

That sounds great until you remember J2’s premium. If J2’s plan costs you $200/month after the employer subsidy, you’re paying $2,400 a year to save copays. The math only works if you have heavy usage. For one or two doctor visits a year, the single-plan setup wins.

The HSA Trap: Why Two Health Plans Can Cost You More Than You Save

This is the part that almost every OE health insurance article skips, and it’s the most expensive mistake you can make.

To contribute to a Health Savings Account, the IRS requires that you be an “eligible individual.” Per IRS HSA eligibility rules in Publication 969, that means:

- You’re covered by a qualifying HDHP on the first day of the month.

- You have no other health coverage that isn’t an HDHP (with narrow exceptions for dental, vision, disability, long-term care, and a handful of “permitted insurance” types).

- You’re not enrolled in Medicare.

- You’re not claimed as a dependent on someone else’s return.

Read the second bullet again. If J1 is an HDHP and you also enroll in J2’s traditional PPO or HMO plan, even as secondary, you are no longer HSA-eligible. The disqualification kicks in for any month in which you have the second coverage, and the calculation flows through to your annual contribution limit on Form 8889.

For 2026, HSA contribution limits are $4,300 for self-only HDHP coverage and $8,550 for family coverage, with a $1,000 catch-up if you’re 55 or older. If you’re in the 32% federal bracket plus a 5% state bracket, a maxed-out self-only HSA contribution shelters about $1,591 in tax. Family coverage roughly doubles that. That tax savings disappears the moment you enroll in J2’s non-HDHP plan.

The math that matters:

- Scenario A: J1 HDHP only. You contribute $4,300 to your HSA. Tax savings around $1,500. You pay J1’s HDHP premium and full HSA-fundable out-of-pocket costs.

- Scenario B: J1 HDHP plus J2 PPO. You can’t contribute to the HSA at all this year. You pay J2 premiums (often $1,800 to $3,600/year after employer subsidy) and lose the $1,500 HSA tax shield. Net cost: roughly $3,300 to $5,100 before counting any benefit J2 actually delivers.

Decision rule we suggest: If J1 is an HDHP and you’re contributing to (or want to contribute to) an HSA, decline J2 health coverage. The HSA tax advantage almost always beats the secondary coverage value unless you have major medical events planned.

One nuance worth knowing: dental and vision plans from J2 are fine. The IRS explicitly lists those as “permitted coverage” that does not disqualify HSA eligibility. So you can take J2’s dental and vision without breaking the HSA.

The 4 OE Insurance Scenarios

OE setups fall into a small number of configurations. Here’s the playbook for each.

| OE Config | Suggested Approach | HSA Compatible? | Key Consideration |

|---|---|---|---|

| W2 + W2 (similar plans) | Keep J1 plan, decline J2 health coverage. Take J2 dental/vision if better. | Yes, if J1 is an HDHP | Simplicity wins; J2 premium savings flow to take-home pay. |

| W2 + W2 (J2 has much better coverage) | Switch primary to J2 at next open enrollment, decline J1 health coverage. | Yes, if you keep only the HDHP side | Don’t run both long-term unless you have heavy usage. |

| W2 + 1099 contractor | Keep W2 plan. Skip marketplace coverage; you already have employer insurance. | Yes, if W2 plan is an HDHP | Self-employed health insurance deduction doesn’t apply when you have employer coverage available. |

| 1099 + 1099 (no W2) | ACA marketplace plan or spouse’s plan. Deduct premiums via Schedule 1. | Yes, if you buy an HDHP-qualified plan | Full premium deduction reduces both income tax and self-employment tax through the proper line. |

What to Do if You’re 1099 or a Contractor

If neither of your jobs is W2, no one is offering you health insurance. The trade-off is that you have full control over which plan you buy and a meaningful tax deduction to offset the premium.

Your options:

- ACA marketplace for self-employed coverage. Healthcare.gov (or your state exchange) lets you compare bronze, silver, gold, and platinum plans. If your projected net self-employment income falls under the threshold, you may qualify for premium tax credits that reduce monthly cost.

- A spouse’s employer plan. Often the cheapest option if it’s available, since employer subsidies typically beat marketplace economics.

- COBRA from a former W2 job. Useful as a short bridge if you recently left employer coverage. You pay the full premium plus a 2% admin fee, so it’s expensive, but it keeps your network and deductible progress intact.

Two tax features matter for 1099 OE practitioners:

- Self-employed health insurance deduction. 100% of premiums you pay for yourself, your spouse, and dependents are deductible as an adjustment to income on Schedule 1 (currently line 17). This is an above-the-line deduction, so you get it whether or not you itemize.

- HSA when self-employed. If you buy an HDHP-qualified marketplace plan, you can open an HSA at any major brokerage and contribute up to the annual limit. There’s no employer matching, but the deduction is yours regardless.

Timing: When Health Insurance Decisions Matter in OE

You can’t switch plans whenever you want. The system runs on three timing windows:

- Annual open enrollment. Most employer plans open enrollment in October or November for a January 1 effective date. ACA marketplace open enrollment typically runs November 1 to January 15 in most states. This is when you can add, drop, or switch coverage with no questions asked.

- Qualifying life events. Starting a new job triggers a 30 to 60 day window to enroll in employer benefits. Losing other coverage triggers a Special Enrollment Period on the marketplace. Marriage, birth, and adoption also qualify.

- Leaving a job. If J1 ends and you want to keep that plan, COBRA lets you stay on it for up to 18 months at full cost plus 2%. Alternatively, job loss is a qualifying event for ACA marketplace enrollment, which is usually cheaper than COBRA if you qualify for premium tax credits.

One overlooked point for OE: starting J2 is itself a qualifying event. You don’t have to wait for open enrollment to enroll in or decline J2’s plan, but you do have to act inside the window your J2 HR specifies, usually 30 days from hire.

FAQ

Can I have two health insurance plans at the same time?

Yes. There’s no law against carrying two employer plans simultaneously. The plans coordinate benefits, with one acting as primary and the other as secondary. The question isn’t whether you can, it’s whether the math justifies the second premium.

Does J2 find out I have insurance from J1?

Not in any way that matters. Enrollment forms don’t ask. Insurance carriers may share data through coordination of benefits queries when claims are filed, but that data goes to the carriers, not to your HR department. There is no employer-visible “you have other insurance” flag tied to your job. The legal considerations of overemployment are mostly about contracts and conflicts of interest, not insurance enrollment.

Can I have an HSA with two health plans?

Only if both plans are HSA-qualified HDHPs and nothing else disqualifies you. In practice, almost no one is enrolled in two HDHPs at the same time. If one job’s plan is a traditional PPO or HMO and you enroll in it on top of your HDHP, you lose HSA eligibility for every month you have the second coverage. Dental and vision plans are fine and don’t break HSA eligibility.

What happens to my health insurance if I leave J1?

You have a few options. COBRA lets you keep the J1 plan for up to 18 months at full cost. If you have J2 already, you can switch J2 from secondary to primary immediately, since job loss is a qualifying event. If J2 is also gone, you can buy ACA marketplace coverage during your Special Enrollment Period. We suggest comparing COBRA and marketplace pricing carefully; marketplace plans with premium tax credits usually beat COBRA on price.

Can I cover dependents under multiple plans?

Yes. Children can be covered by both parents’ plans, and the birthday rule determines which is primary. For OE, this means if both you and your spouse have employer coverage, your kids could be on both, with one primary and one secondary. The same coordination of benefits math applies: you’re paying two premiums for marginal additional benefit unless your family has high medical usage.

What are my health insurance options if both my jobs are 1099?

You’re shopping the individual market. Start with healthcare.gov (or your state exchange), estimate your annual net self-employment income honestly, and compare metal tiers. If you’re healthy and want maximum tax efficiency, pair an HDHP-qualified bronze plan with a self-directed HSA. Deduct 100% of your premiums on Schedule 1. If you’re on the edge of premium tax credit eligibility, talk to a tax pro before locking in a plan, since the credit math interacts with the self-employed deduction in non-obvious ways.

The OE community spends a lot of energy optimizing 401(k) contributions, RSU strategies, and tools for managing multiple remote jobs. Health insurance deserves the same attention. Pick the plan that fits your usage pattern, protect HSA eligibility if you have an HDHP, and don’t carry a second premium just because you can.